Press Releases

- Article

APAC Education Industry Report H1 2020

September 18, 2020

Introduction

We are pleased to share with you a summary update of market valuations and activities in the Asia Pacific education services industry for the first half of 2020.

Education is one of the key sectors in which Armor specializes in and closely follows market trends. Please contact us for further discussion.

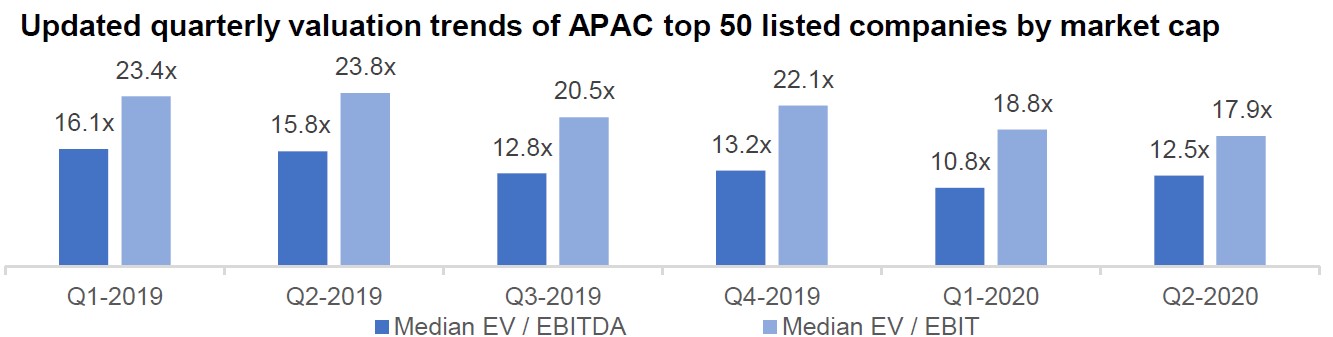

Valuations of Asia Pacific’s public companies fluctuated over last 6 quarters ending June 2020. H1-2020 was characterized by lower multiples, EBITDA multiples were almost 33% lower by the end of Q1-2020 (10.8x in Q1-2020 vs 16.1x in Q1-2019) and almost 21% by end of Q2-2020 (12.5x in Q2-2020 vs 15.8x in Q2-2019).

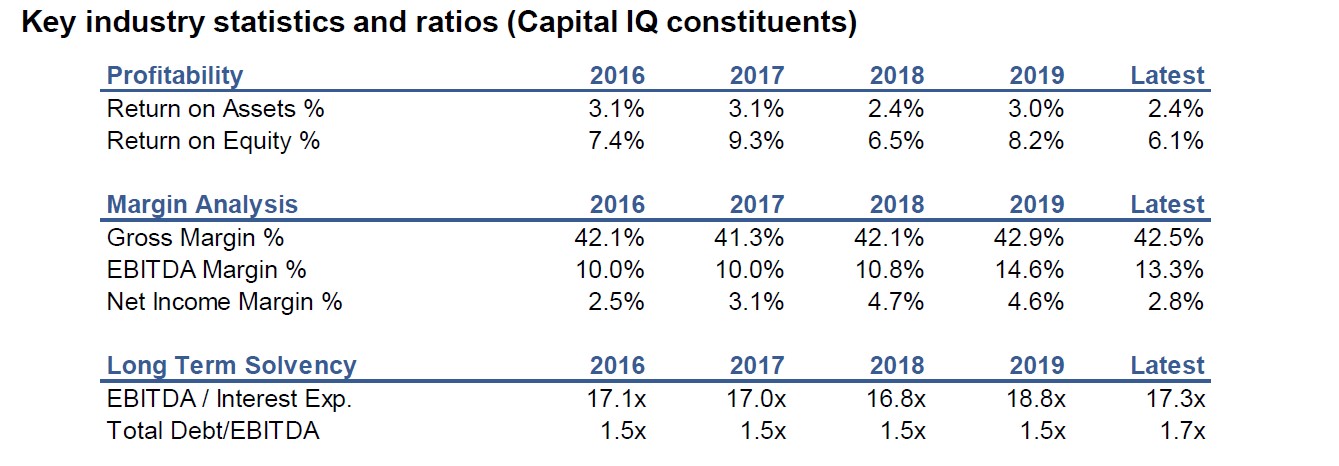

Based on around 130 selected companies, the table above illustrates that industry returns and margins have been decreasing over the last eight months (latest values) in comparison with 2019.

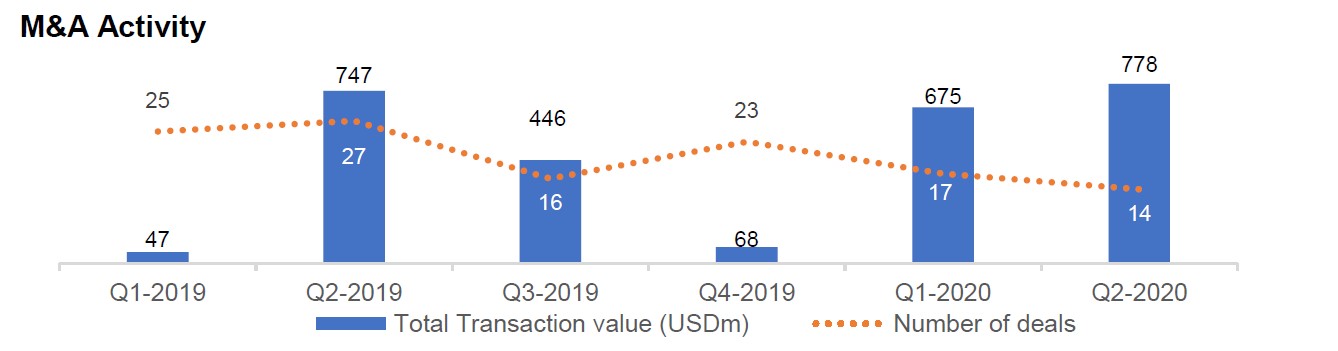

Overall, first half of 2020 was characterised by lower M&A deal count, while total transaction value continue to show large fluctuations and is pushed up by a few large deals (e.g. China Distance Education – EV USD 284.3m).

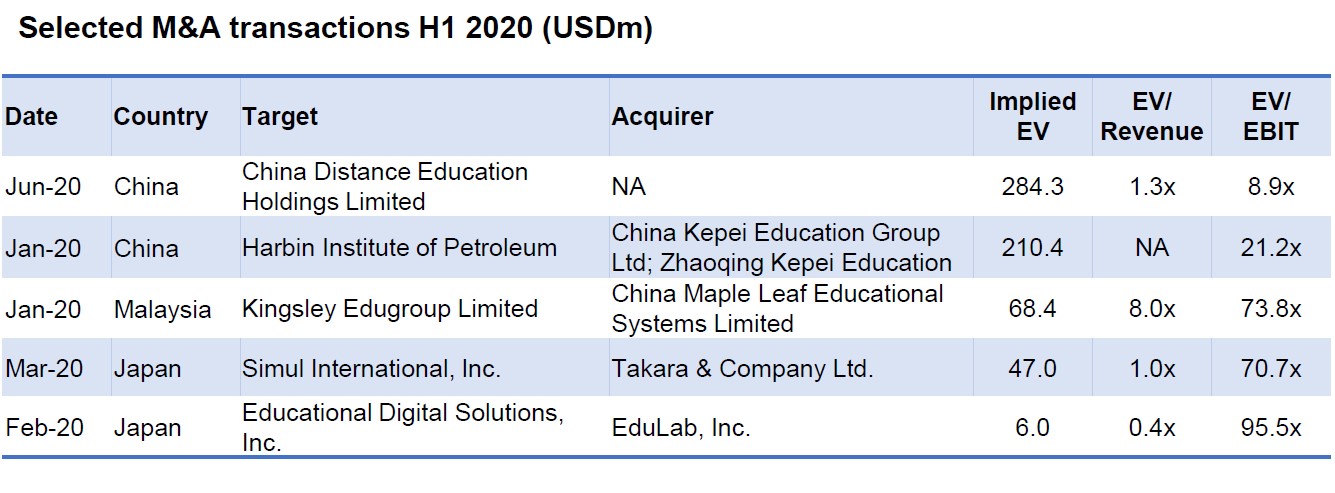

Armor selected the largest M&A transactions across the region in 2020 H1 for which information on Implied Enterprise Value (EV) was available. Two transactions stand out, the acquisition of China Distance Education and the acquisition of Harbin Institute of Petroleum.

Education is one the key sectors in which Armor specializes and closely follows market trends.

Please contact us for an in-depth discussion via enquiry@armor-capital.com