Press Releases

- Article

Directors’ Duties in a “Desperate” IPO Market

July 25, 2022

By Frederick Chann

After a very quiet Q4 2021 and Q1 2022, and in spite of a continually weak and volatile market, 21 IPOs were launched in Q2 2022. All but five were announced in the last 10 days of the quarter, just before the requirement for the inclusion of H1 2022 financial data kicked in.

In this article, we look at the anatomy and consequences of a “desperate” IPO market. We also review directors’ duties to shareholders and investors. Those are the same in any market environment, but take on much greater significance in challenging times, especially for independent non-executive directors (“INEDs”).

Anatomy of a “Desperate” IPO Market

Broad Market Weakened Significantly – Fast!

- The Hang Seng Index (“HSI”) declined close to 30% since June 30, 2021.

Underwriting Revenues Dried Up

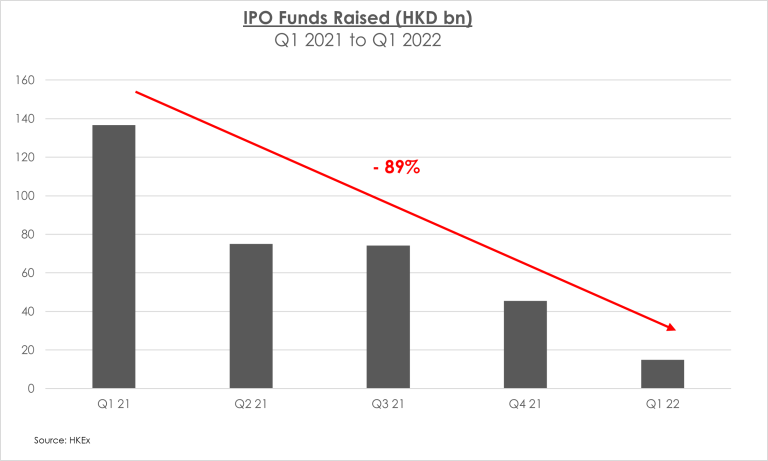

- IPO funds raised dropped in Q1 2022 by two-thirds from Q4 2021 and close to 90% from the year prior (source: HKEx).

- Underwriters needed to close deals to bring in much needed revenue …. and keep their jobs!

Significant Backlog Built Up

- By the end of Q1 2022, there were over 150 active IPO applicants (source: HKEx).

- These companies needed capital to fund their growth and / or extend their cash runways (i.e. survival).

- If they waited till after June 30, they would have had to refresh their financials which would take 6-8 weeks.

What Transpired? Disasters!

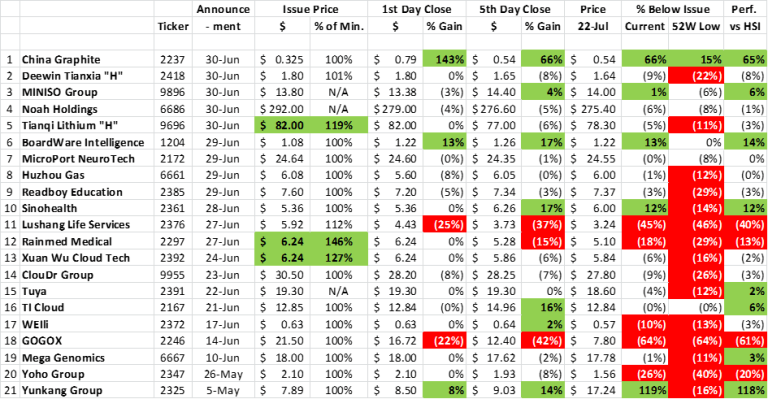

During Q2 2022, 21 IPOs were launched.

- All but two were announced during or after the second week of June. Traffic jam!

- 16 provided a pricing range – three quarters of those were eventually priced at or very near to the bottom.

- In spite of that, only 5 (i.e. less than a quarter) are trading above issue (see Appendix).

- Only 8 (i.e. just 38%) are outperforming the benchmark HSI.

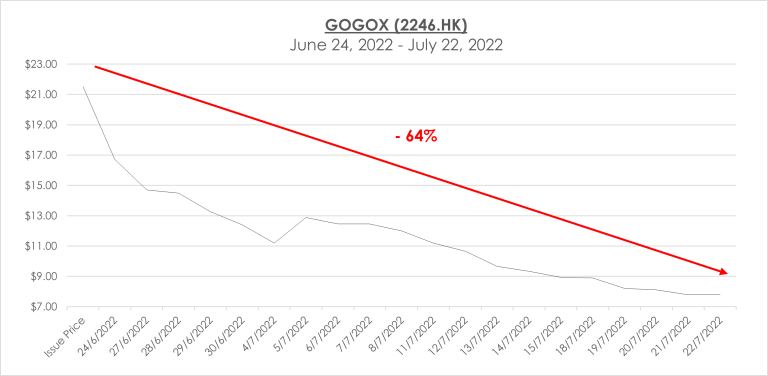

- GOGOX, which launched its IPO relatively early, saw its share price dive 22% on the first day and 42% by the end of the first week!

- That first trade took place on June 24 – 5 days before the next deal was priced. Way to set the tone for the 17 that followed!

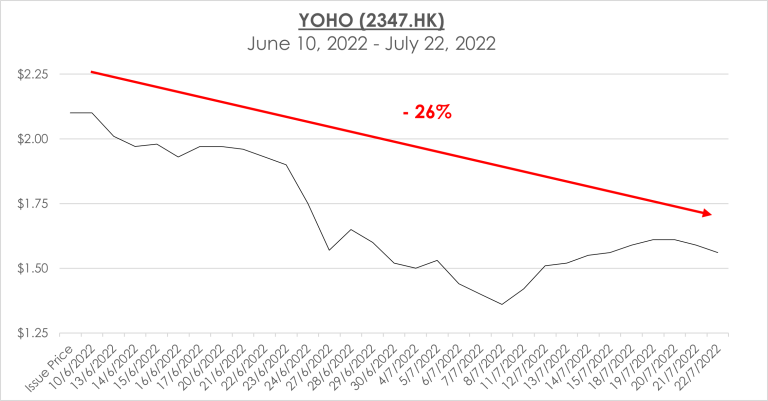

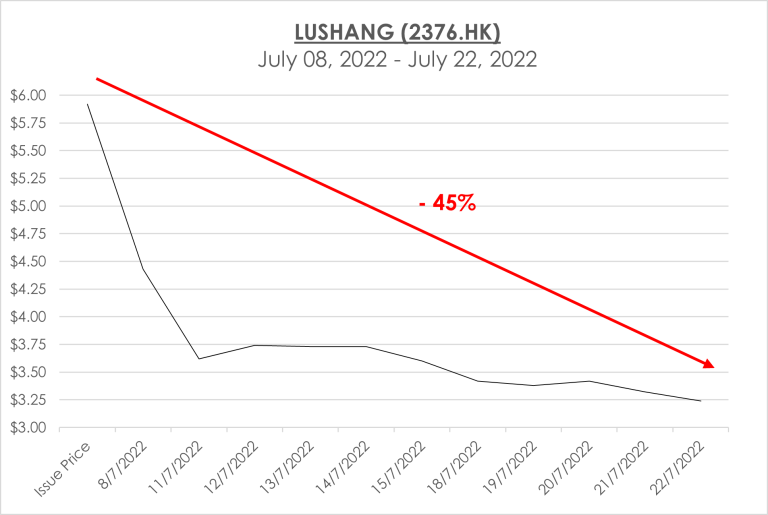

- In merely weeks, three companies lost 26% (Yoho 2347.HK), 45% (Lushang Life Science 2376.HK) and 64% (GOGOX 2246.HK) of their respective market values!

Directors' Duties

Should directors of these companies have anticipated this?

- Absolutely!

- Perhaps not the exact magnitude, but they certainly should have had a good sense of the overall market and importantly, what the reasonable ranges of valuation would have been for their respective companies.

- Besides having conducted their own due diligence, they should (and would) have consulted with the lead underwriters.

What are directors’ duties to existing shareholders and prospective investors?

- Directors – executive, non-executive and INEDs – all have fiduciary responsibilities to all shareholders. It is a balancing act!

- Fiduciary” has both a legal and ethical element. “Trust” and “prudence” are often included in its definition.

- In the cases cited above, it is hard to argue that their directors had fulfilled their fiduciary duties.

Why is the role of INEDs unique and so critical in a “desperate” market environment?

- As discussed earlier, in such instances, companies are racing against the clock, desperate to raise funds. Underwriters are desperate to close deals and bring in much needed revenue.

- So who are there to act for and protect the minority shareholders, including new investors? INEDs!

What should INEDs be doing?

- Do your own due diligence.

- Seek and document professional advice.

- Apply independent judgement.

- Speak up at board meetings.

- Last resort – resign!

Final Thoughts

If this had taken place in a more litigious market like the US,

- class action lawsuits would have been filed left, right and centre, against not just the companies, but individual board directors and underwriters as well!

- the Securities & Exchange Commission would be breathing down their necks.

I would be most disappointed if the Securities & Futures Commission does not at least launch preliminary investigations into the more notable disasters. It does not bode well for the Hong Kong market.

Individual investors who should often wonder if they will be represented well,

- do your own homework – read the prospectus, starting with the “Risk Factors” section

- due diligence the directors, especially the INEDs

Board directors of IPO companies which have seen quick and significant de-valuations,

- going forward, how much higher will the premiums for your companies’ directors’ and officers’ liability insurance be?

- how long will it take before your companies can return to the market and raise capital?

- how long will it take for you to recover your personal reputation?

Fred is a Director & Senior Advisor at Armor Capital. He advises C-suite executives and boards of directors on strategy development and planning, corporate governance, equity & debt financings, IPO preparation and M&A due diligence. In his consultancy practice, he draws upon two decades of experience in investment banking, fund management and entrepreneurship. Fred has also served on the boards of listed and private companies as well as NGOs, in capacities including Chair, Governance Committee & CFO. For 10 years, he was a Fellow of the Hong Kong Institute of Directors. He received both his BA (Hons.) & MBA (Dean’s Honour List) from the Ivey Business School (Canada).

fred@armor-capital.com / +852 9686 5928

Appendix

Disclaimer:

No part of this publication may be reproduced or transmitted in any form or for any purpose without the express permission of Armor Capital. These materials are provided by Armor Capital for informational purposes only, without representation or warranty of any kind, and Armor Capital shall not be liable for errors or omissions with respect to the materials. Armor Capital declines any liability in relation to this information, nor shall it be liable for any decisions taken based on the information contained on this publication.